Platform Strategy

Many companies treat platforms as a feature bolted onto an existing pipeline business. The result is a confused product that does neither role well, leaves capital trapped, and exposes the firm to faster-moving rivals. This framework guides leaders through the full platform shift across model design, network effects, cold-start launch, transition planning, and governance, so the move from linear value chain to many-sided ecosystem follows a deliberate sequence.

Platforms now reshape competitive dynamics across every industry where they appear, but the failure rate stays high. BCG Henderson Institute research found that fewer than 15 percent of business ecosystems prove sustainable in the long run, with weak governance the single most common cause of failure. The gap between platform winners and traditional incumbents has continued to widen, and ecosystem design has become a primary lever of competitive strategy.

How to Choose a Platform Model

Platform strategy begins with one decision: what kind of platform does the business want to be. The foundations section forces this decision into the open. Pipeline businesses control a linear value chain and capture margin on each step, with revenue tied directly to product sales. Platform businesses orchestrate exchanges between many participants and capture a share of value created by others, with revenue tied to take rates, access fees, or advertising. The two require different cost structures, different talent, and different metrics. Leaders that confuse the two ship features that satisfy neither audience and leave capital trapped in the wrong investments.

Van Alstyne, Parker, and Choudary, the authors of Platform Revolution, observed in Harvard Business Review that in 2007 the five largest mobile phone makers controlled 90 percent of industry profits. By 2015, Apple's iPhone captured 92 percent of global handset profits while four of the five legacy leaders made no profit at all. The shift came from one strategic move: Apple paired a pipeline product with the App Store, a platform that connected developers and users. A strategic positioning matrix in the framework plots platforms on two axes, value created and value captured, so teams can place rivals in the four resulting quadrants and understand where the business currently sits.

The platform models slide closes the foundations section with four archetypes that map to revenue logic. Transaction platforms like Uber, Airbnb, eBay, and DoorDash match buyers and sellers and earn a take rate on each transaction. Innovation platforms like Stripe, AWS, Salesforce, and iOS let third-party developers build complements on shared infrastructure. Hybrid platforms like Microsoft, Amazon, Google, and Apple combine the two layers under one roof. Content platforms like Spotify, Substack, TikTok, and YouTube connect creators with audiences and monetize attention or subscriptions. Managers use this matrix to test which model fits the company's assets, customers, and capital position before any build work begins.

Build Network Effects as the Moat

Network effects determine whether a platform compounds advantage or erodes into a commodity. The defensibility section breaks the topic into four specific types: direct (same-side), indirect (cross-side), data (algorithmic), and local (geographic). Each type behaves differently under stress and demands its own investment plan. Managers that treat network effects as a single undifferentiated concept end up with weak engagement, low density, and rivals that pick off users one segment at a time. A precise vocabulary turns abstract talk about moats into concrete bets the team can fund, measure, and defend.

Andrew Chen, the former head of rider growth at Uber and author of The Cold Start Problem, observed that few software products reach a billion active users and that nearly all of them rely on at least one type of network effect. Chen distinguishes the early-stage cold-start phase from the later tipping-point and saturation phases, and notes that platforms with the wrong network-effect investments at each stage either fail to gain density or hit a ceiling. The framework converts this insight into a four-quadrant grid where each effect type carries a specific budget allocation, a specific action, and a specific KPI shift, so the investment plan flows directly from the network-effect diagnosis.

A multi-homing risk quadrant follows. The axes are switching cost and cost to multi-home. Platforms with low switching cost and low multi-home cost sit in the high-risk commodity zone, where rivals replicate the service quickly. Platforms with high switching cost and high multi-home cost (Apple iOS, AWS, Salesforce, Stripe) sit in the defensible monopoly zone. The framework lists named examples in each quadrant so teams can position the business honestly and decide whether to invest in lock-in features, exclusive content, or proprietary data before competition tightens.

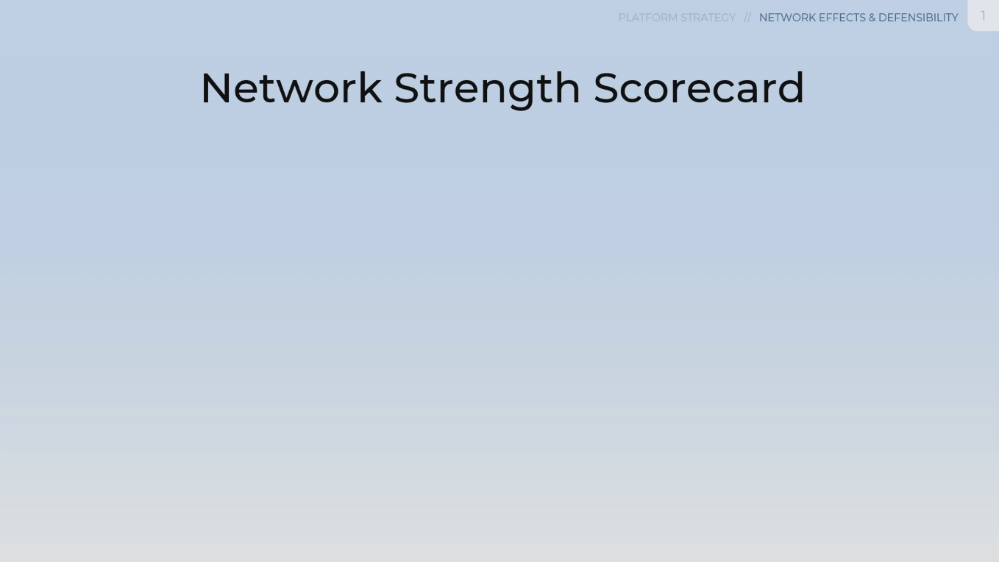

The network strength scorecard closes the section with six metrics that quantify defensibility: engagement rate, same-side density, cross-side multiplier, time to value, multi-homing index, and monthly churn. Each metric carries a baseline and a target movement, which lets the executive team track network health alongside revenue. Bakos and Halaburda found in Management Science that when both sides multi-home, the standard advice to subsidize one side breaks down, which makes a clean scorecard even more important for the pricing decisions that follow.

How to Solve the Cold-Start Problem

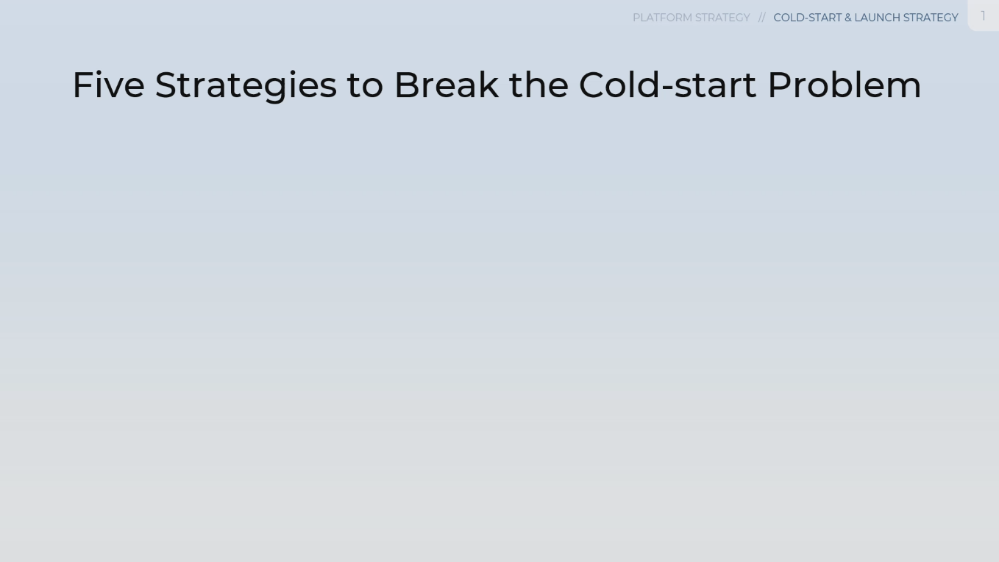

Platforms fail at launch when neither side shows up. The cold-start section addresses this chicken-and-egg problem head on. Five named strategies sit at the core: subsidize one side to attract the other, piggyback on another network's users, pick a narrow wedge as a beachhead, simulate matching manually until real supply arrives, and seed one side with proprietary supply. Each strategy carries a clear use case, a real-world precedent, and an honest assessment of cost and risk. Leaders that pick a strategy by default rather than deliberation often waste a year on the wrong tactic before they course-correct.

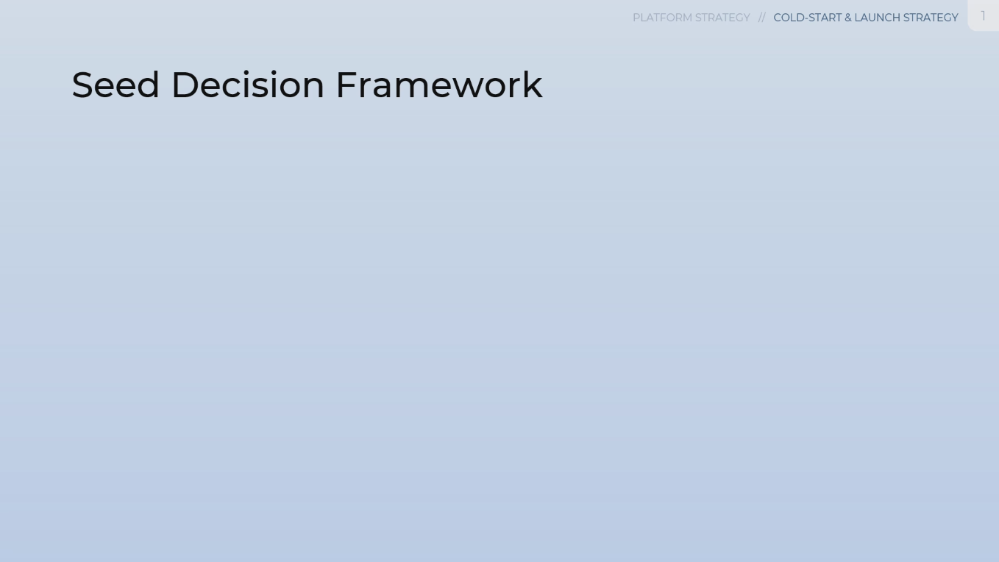

A seed decision framework helps teams answer the deeper question of which side comes first. The framework compares demand-side and supply-side starts across six dimensions: acquisition cost, quality control, time to liquidity, scale challenge, best-for use case, and anchor examples. Tinder seeded users first because consumer marketplaces benefit from demand-side liquidity. Etsy seeded sellers first because B2B marketplaces and vertical SaaS need vetted supply. The rule of thumb is straightforward: seed the side with higher quality variance, because bad participants damage the network most on that side and recovery becomes expensive.

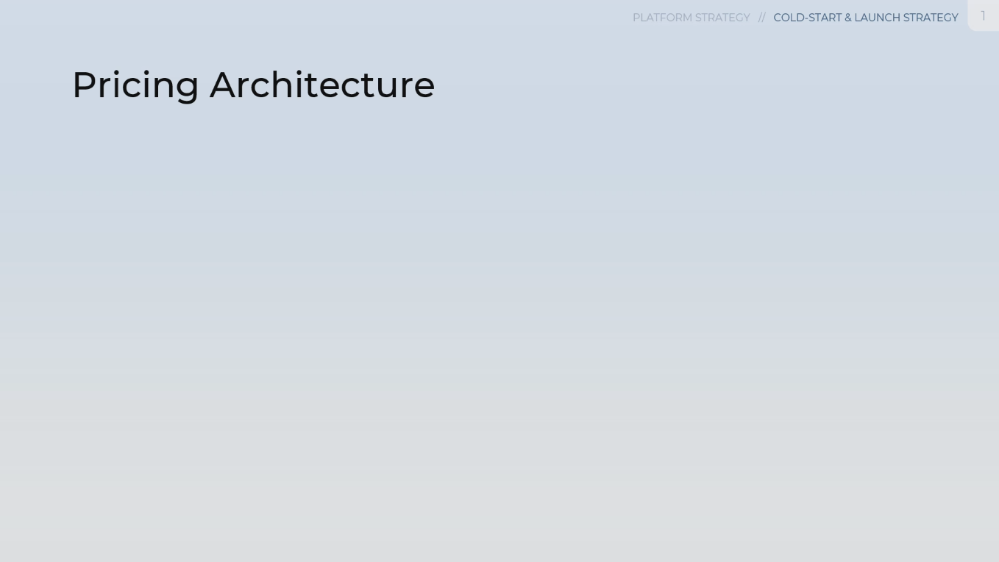

Pricing architecture is the third lever. The seminal work of Rochet and Tirole established in the Journal of the European Economic Association that in two-sided markets, the structure of prices, and not just the level, determines participation on each side and the platform's total profit. The framework slide makes this concrete with seven examples. Uber subsidizes drivers and earns roughly 25 percent take rate from riders. OpenTable charges restaurants one dollar per cover and lets diners book for free. LinkedIn keeps job seekers free and charges recruiters about eleven thousand dollars per seat per year. The pattern is consistent: the platform monetizes the side with higher willingness to pay and subsidizes the side that creates the network effect for the other.

A marquee user acquisition checklist closes the cold-start section. The checklist organizes work into four streams: supply-side marquees, demand-side marquees, launch sequencing, and quality signals. Specific items cover twenty-four-month exclusivity with a seed cohort, five anchor logos in the target ICP, a verified-badge program with public criteria, and case studies within sixty days of go-live. The checklist gives teams a concrete week-by-week plan rather than a vague aspiration to recruit prestige users.

How to Plan the Pipeline-to-Platform Transition

Most incumbents that attempt the platform shift treat it as a software project. They build an API, publish documentation, and wait for partners to integrate. The transition fails because the operating model behind the linear value chain does not change. The transition section in this framework forces the conversation onto the right plane. It maps the shift as a multi-quarter sequence with named milestones, partner counts, and KPI gates, then catalogs the seven operating-model dimensions that must shift in parallel. A staged transition reduces leadership fatigue and protects the legacy business while new revenue streams ramp.

The transition plan in the framework unfolds across four phases. The first phase, Validate and Recruit, covers Q1 to Q2 2026 with a soft pilot of five partners, an API spec at version 0.1, and identification of partner candidates. The second phase, Open Beta in Q3 2026, ships the public API and sandbox, publishes governance version 1, and onboards twenty-five partners. The third phase, Scale, runs from Q4 2026 to Q1 2027 with self-serve onboarding, a dispute and SLA system, and more than one hundred partners live. The final phase, Optimize, launches a dynamic pricing engine, a premium tier, and an ecosystem fund. Four KPIs track progress across all phases: signed partners, active integrations, marketplace GMV, and stable take rate.

The operating model shift slide identifies seven dimensions that move from pipeline to platform: value architecture from linear chain to many-to-many ecosystem, integration from outbound demand to two-sided recruitment, quality control from inspection to reputation systems, revenue model from product sales to take rate, scaling from capacity additions to user additions, customer relations from transactional to bidirectional, and marketing from vertical ownership to horizontal orchestration. Each dimension forces a parallel organizational change and a parallel skill rebuild, which McKinsey research on platform transformation has identified as the most common point of failure.

A trajectory chart visualizes the shift from pipeline to platform across four stages: launch, beachhead, expansion, and steady-state. The platform line crosses the pipeline line at the beachhead stage and accelerates from there, with the cross-side multiplier reaching 3.4 times at steady-state. Leaders use this curve to set realistic expectations with boards and investors who often expect pipeline-style linear growth from a platform that needs critical mass first. The early dip below the pipeline line is structural, not a sign of weak execution.

How to Govern and Defend the Platform

Platform governance shapes scale, control, and economics simultaneously. The openness matrix in the framework plots a platform on two axes: supply-side openness and demand-side openness. The four quadrants name the resulting models. Open platform sits open on both sides, with maximum scale and lowest control. Federated keeps open contributors with restricted access. Curated marketplace combines open users with vetted suppliers. Walled garden stays closed on both sides for premium experience. Each quadrant carries four scorecard dimensions: scale potential, ecosystem speed, quality control, and monetization control.

A governance engine slide breaks the rule set into four explicit categories. Rules of entry cover KYC and identity verification, onboarding SLA targets, background or credit checks, and quality standards. Rules of exchange define pricing controls, refund and chargeback policy, dispute flow, and take-rate transparency. Rules of evolution publish API versioning, deprecation timelines, a public change log, and a partner advisory board. Rules of exit set off-platform contact rules, data portability standards, notice periods, and reputation transferability. The four categories together form the governance contract that participants accept when they join.

A coopetition map plots partners and rivals across two axes: ecosystem synergy and competition intensity. Pure allies sit in the high-synergy, low-competition quadrant. Adjacent players sit in the low-synergy, low-competition quadrant. Frenemies sit in the high-synergy, high-competition quadrant, with named examples like Netflix and Disney plus, Spotify and Apple, or Slack and Microsoft. Direct rivals sit in the low-synergy, high-competition quadrant. The map turns ambiguous ecosystem relationships into specific commercial postures the partnership team can act on.

Platform encroachment is a permanent risk for any company that sits on top of another platform. Eisenmann, Parker, and Van Alstyne identified platform envelopment in the Strategic Management Journal as a strategy where one platform enters another's market by bundling shared user relationships, which lets the attacker harness network effects that previously protected the incumbent. The safeguards slide names six risk factors that drive encroachment likelihood: customer relationship depth, strategic value to the platform owner, data visibility, adjacent capabilities, margin attractiveness, and substitutability. It then lists five defensive plays: diversify across platforms, own the customer relationship, build proprietary data moats, invest beyond replication, and engage in advocacy and policy.

A risk reduction trajectory shows how the five defensive plays compound. The chart starts at today's composite risk level. Each defensive play stacks on the next: diversify across platforms, own the customer, build a data moat, differentiate beyond replication, and invest in policy. The cumulative effect drops composite risk by 60 percent over the defensive build sequence. The chart gives the executive team a visual case for the order of investments rather than a flat list of priorities.

The risk and response slide closes the section with a structured plan across five risk categories. Platform encroachment shows high likelihood with the response of activating the defensive playbook and diversifying GMV mix. Marquee partner defection shows medium likelihood and triggers a customer-success swat team when a top-ten partner volume drops more than 20 percent month over month. Multi-homing acceleration triggers lock-in features and an exclusive content tier when the multi-homing index exceeds 35 percent. Quality and trust failure triggers a verified-supplier program and a tighter dispute SLA when NPS drops more than ten points. Take-rate compression triggers tiered pricing and a premium services bundle when the effective take rate falls below 11 percent.

Platform strategy is not a single decision but a sequence of decisions made under uncertainty. Each choice in the sequence locks the next set of choices, so early errors compound. Model selection narrows the design space. Network-effect investments define the moat. Cold-start tactics determine whether the platform reaches density at all. The transition plan controls execution risk during the shift. Governance and defense protect what gets built from rivals and from regulators. Companies that treat these decisions as a single coherent agenda outperform companies that treat each one in isolation.

The platforms that dominate the next decade will not be the ones with the best technology. They will be the ones whose leadership team has internalized the discipline of orchestration, the patience required to seed a network, and the rigor to govern an ecosystem at scale. Mastery of platform strategy turns scattered tactical bets into a single compounding system of advantage.